At ERA Leatherman Realty, we believe in embracing diversity and celebrating the vibrant cultures that enrich our community. 🌎🇺🇸

As a real estate broker and property manager in Florence, South Carolina, I’ve had the privilege of working with individuals from various backgrounds. Hispanic Heritage Month gives everyone an opportunity to recognize the incredible contributions and traditions of the Hispanic community.

From the warmth of their hospitality to the exquisite flavors of their cuisine, Hispanic culture has left an indelible mark on our lives and our city. I’m so grateful for the chance to learn from our Hispanic friends and neighbors.

Let’s take this month to honor and appreciate the heritage and achievements of the Hispanic community.

Together, we celebrate the diversity that makes us stronger. 🤝

Toward the end of last year, there were a number of headlines saying home prices were going to fall substantially in 2023. That led to a lot of fear and questions about whether there was going to be a repeat of the housing crash that happened back in 2008. But the headlines got it wrong.

While there was a slight home price correction after the sky-high price appreciation during the ‘unicorn’ years, nationally, home prices didn’t come crashing down. If anything, prices were a lot more resilient than many people expected.

Let’s take a look at some of the expert forecasts from late last year stacked against their most recent forecasts to show that even the experts recognize they were overly pessimistic.

Expert Home Price Forecasts: Then and Now

This visual shows the 2023 home price forecasts from seven organizations. It provides the original 2023 forecasts (released in late 2022) for what would happen to home prices by the end of this year and their most recently revised 2023 forecasts (see chart below):

As the red in the middle column shows, in all instances, their original forecast called for home prices to fall. But, if you look at the right column, you’ll see all experts have updated their projections for the year-end to show they expect prices to either be flat or have positive growth. That’s a significant change from the original negative numbers.

There are a number of reasons why home prices are so resilient to falling. As Odeta Kushi, Deputy Chief Economist at First American, says:

“One thing is for sure, having long-term, fixed-rate debt in the U.S. protects homeowners from payment shock, acts as an inflation hedge – your primary household expense doesn’t change when inflation rises – and is a reason why home prices in the U.S. are downside sticky.”

A Look Forward To Get Ahead of the Next Headlines

For home prices, you’re going to continue to see misleading media coverage in the months ahead. That’s because there’s seasonality to home price appreciation and they’re going to misunderstand that. Here’s what you need to know to get ahead of the next round of negative headlines.

As activity in the housing market slows at the end of this year (as it typically does each year), home price growth will slow too. But, this doesn’t mean prices are falling – it’s just that they’re not increasing as quickly as they were when the market was in the peak homebuying season.

Basically, deceleration of appreciation is not the same thing as home prices depreciating.

Bottom Line

The headlines have an impact, even if they’re not true. While the media said home prices would fall significantly in their coverage at the end of last year, that didn’t happen. Let’s connect so you have a trusted resource to help you separate fact from fiction with reliable data.

Mortgage Rates: Past, Present, and Possible Future

If you’re hoping to buy a home this year, you’re probably paying close attention to mortgage rates. Since mortgage rates impact what you can afford when you take out a home loan – and affordability is a challenge today – it’s a good time to look at the big picture of where mortgage rates have been historically compared to where they are now. Beyond that, it’s important to understand their relationship with inflation for insights into where mortgage rates might go in the near future.

Giving Context to the Sticker Shock

Freddie Mac has been tracking the 30-year fixed mortgage rate since April of 1971. Every week, they release the results of their Primary Mortgage Market Survey, which averages mortgage application data from lenders across the country (see graph below):

Looking at the right side of the graph, mortgage rates have increased significantly since the start of last year. But even with that rise, today’s rates are still below the 52-year average. While that historical perspective is good context, buyers have gotten used to mortgage rates between 3% and 5%, which is where they’ve been over the past 15 years.

That’s important because it explains why the recent jump in rates might have you feeling sticker shock even though they’re close to their long-term average. While many buyers have adjusted to the elevated rates over the past year, a slightly lower rate would be a welcome sight. To determine if that’s a realistic possibility, it’s important to look at inflation.

Where Could Mortgage Rates Go in the Future?

The Federal Reserve has been working hard to lower inflation since early 2022. That’s significant because, historically, there’s been a connection between inflation and mortgage rates (see graph below):

This graph shows a pretty reliable relationship between inflation and mortgage rates. Looking at the left side of the graph, each time inflation moves significantly (shown in blue), mortgage rates follow suit shortly after (shown in green).

The circled portion of the graph points out the most recent spike in inflation, with mortgage rates following closely behind. As inflation has moderated a bit this year, mortgage rates haven’t yet made a similar move.

That means, if history is any guide, the market is waiting for mortgage rates to follow inflation and head back down. It’s impossible to accurately predict where mortgage rates will go for sure, but moderating inflation means mortgage rates going down in the near future would fit a well-established trend.

Bottom Line

To understand where mortgage rates may be going, it’s helpful to look at where they’ve been in the past. There’s a clear connection between inflation and mortgage rates, and if that historical relationship holds true, the recent decline in inflation may mean good news for the future of mortgage rates and your homeownership goals.

Have you been trying to buy a home, but higher mortgage rates and home prices are limiting your options? If so, here’s some good news – based on what Ali Wolf, Chief Economist at Zonda, has to say – smaller, more affordable homes are on the way:

“Buyers should expect that over the next 12 to 24 months there will be a notable increase in the number of entry-level homes available.”

In some ways, smaller homes are already here. When the pandemic hit, the meaning of home changed. People needed the space their home provided not only as a place to live, but as a place to work, go to school, exercise, and more. Those who had that space were more likely to keep it. And those that didn’t were in a position where they were trying to sell their smaller house to move up to a larger one. That meant the homes coming to the market during the pandemic were smaller than those on the market before the pandemic – and that trend continues today (see graph below):This graph also shows how the size of homes on the market changes seasonally. Larger homes tend to come on the market during the summer months when households with children who are out of school are looking to move.

That seasonality means, based on historical trends and the fact that fall is now approaching, we can expect smaller, more affordable homes to come to the market throughout the rest of the year.

That’s great news because, as Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB), states, the need for these types of homes has gone up recently:

“. . . as interest rates increased in 2022, and housing affordability worsened, the demand for home size has trended lower.”

What Does This Mean for You?

The seasonal trend of smaller homes coming to the market in the later months of the year, coupled with builders bringing smaller, more affordable newly built homes to the market right now, is good news – especially if you’re finding it difficult to afford a home. Mikaela Arroyo, Director of the New Home Trends Institute at John Burns Real Estate Consulting, says this about a potential increase in the availability of smaller homes:

“It’s not solving the affordability crisis, but it is creating opportunities for people to be able to afford an entry-level home in an area.”

Bottom Line

If a smaller, more affordable home sounds appealing to you, good news – they’re coming. To keep up with what’s available in our area, let’s connect.

According to the Humane Society of the United States, “Many people enjoy the booming sounds and flashing colors of fireworks, but they can be terrifying, overwhelming and hazardous for both wild and domestic animals. On the Fourth of July, many animals become so frightened by the noise and commotion of fireworks that they run from otherwise familiar environments and people, and sadly become lost. They may also suffer devastating or even fatal health effects from the stress. The sudden bright flashes and sounds can cause wild animals to run into roadways, resulting in more car accidents than normal. Wildlife rehabilitation centers are often flooded with traumatized, injured and orphaned wild animals after the holiday.”

Where Will You Go If You Sell? Newly Built Homes Might Be the Answer.

Do you want to sell your house, but hesitate because you’re worried you won’t be able to find your next home in today’s market? You’re not alone, but there’s some good news that may ease your worries. New home construction is up and is becoming an increasingly significant part of the housing inventory.

That means when you go to put your house on the market this summer, considering newly built homes is crucial for expanding the options you’ll have for your next move.

Near-Record Percentage of New Home Inventory

Newly built homes today make up a near-record percentage of the total number of homes available for sale (see graph below):

In fact, as the data shows, newly built homes now make up 31% of the total for-sale inventory. Over the past couple of decades, newly built homes made up an average of only around 13% of total housing inventory from 1983 to 2019.

That means the percentage of the total available homes that are newly built is over two times higher than the norm.

Why This Matters to You

Overall, the supply of homes for sale is still low. And when there’s limited supply, it’s crucial to explore all of your available choices. New-home construction has emerged as a game changer with increasing inventory. Not to mention, recent data shows it’s gaining even more momentum as more newly built homes are underway and will be coming to the market in the months ahead.

Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB), highlights the importance of newly built homes for those looking to buy in today’s housing market. Dietz states:

“With limited available housing inventory, new construction will continue to be a significant part of prospective buyers’ search in the quarters ahead.”

Don’t overlook this growing market segment and risk missing out on great opportunities to find your ideal home. Since new home construction accounts for roughly 31% of total for sale inventory, you could be cutting nearly one in three options from your search if you don’t consider newly built homes.

If you’re looking to make a move, a local real estate agent can help you sell your current house and explore newly built options in your area. They have the expertise you need to handle both sides of the process so you can move out of your current house and into your brand-new dream home.

Bottom Line

Now’s the time to sell your house and take advantage of the momentum that’s building in new home construction. Let’s connect so you have a guide throughout the selling and buying process. Together, we can make your transition to a newly built home a reality.

Key Reasons To Use a Real Estate Agent When You Sell [INFOGRAPHIC]

Some Highlights

An agent is a really important part of selling your home because they bring a lot of skill and expertise to the sales process.

They’ll explain what’s happening today, what that means for you, and how to price and market your house. They’re also skilled negotiators and well versed in the contracts and disclosures involved.

Let’s connect to ensure you have an expert helping you sell your house successfully.

Why the Median Home Price Is Meaningless in Today’s Market

The National Association of Realtors (NAR) will release its latest Existing Home Sales (EHS) report later this week. This monthly report provides information on the sales volume and price trend for previously owned homes. In the upcoming release, it’ll likely say home prices are down. This may feel a bit confusing, especially if you’ve been following along and seeing the blogs saying that home prices have bottomed out and turned a corner.

So, why will this likely say home prices are falling when so many other price reports say they’re going back up? It all depends on the methodology of each report. NAR reports on the median sales price, while some other sources use repeat sales prices. Here’s how those approaches differ.

The Center for Real Estate Studies at Wichita State University explains median prices like this:

“The median sale price measures the ‘middle’ price of homes that sold, meaning that half of the homes sold for a higher price and half sold for less . . . For example, if more lower-priced homes have sold recently, the median sale price would decline (because the “middle” home is now a lower-priced home), even if the value of each individual home is rising.”

Investopedia helps define what a repeat sales approach means:

“Repeat-sales methods calculate changes in home prices based on sales of the same property, thereby avoiding the problem of trying to account for price differences in homes with varying characteristics.”

The Challenge with the Median Sales Price Today

As the quotes above say, the approaches can tell different stories. That’s why median price data (like EHS) may say prices are down, even though the vast majority of the repeat sales reports show prices are appreciating again.

Bill McBride, Author of the Calculated Risk blog,sums the difference up like this:

“Median prices are distorted by the mix and repeat sales indexes like Case-Shiller and FHFA are probably better for measuring prices.”

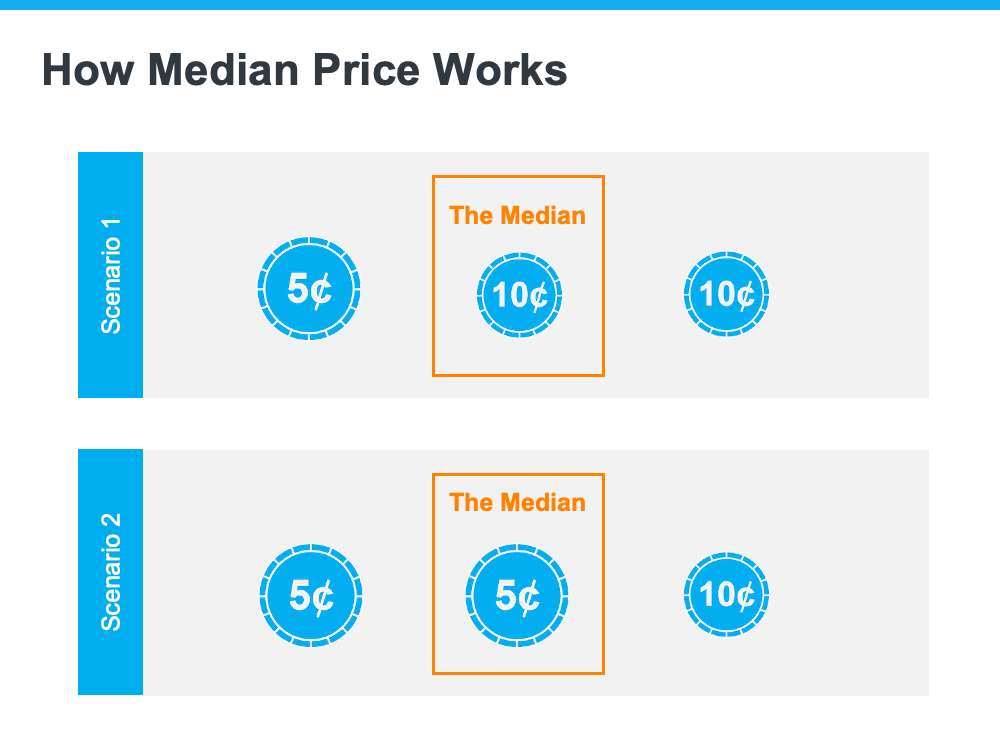

To drive this point home, here’s a simple explanation of median value (see visual below). Let’s say you have three coins in your pocket, and you decide to line them up according to their value from low to high. If you have one nickel and two dimes, the median value (the middle one) is 10 cents. If you have two nickels and one dime, the median value is now five cents.

In both cases, a nickel is still worth five cents and a dime is still worth 10 cents. The value of each coin didn’t change.

That’s why using the median home price as a gauge of what’s happening with home values isn’t worthwhile right now. Most buyers look at home prices as a starting point to determine if they match their budgets. But, most people buy homes based on the monthly mortgage payment they can afford, not just the price of the house. When mortgage rates are higher, you may have to buy a less expensive home to keep your monthly housing expense affordable. A greater number of ‘less-expensive’ houses are selling right now for this exact reason, and that’s causing the median price to decline. But that doesn’t mean any single house lost value.

When you see the stories in the media that prices are falling later this week, remember the coins. Just because the median price changes, it doesn’t mean home prices are falling. What it means is the mix of homes being sold is being impacted by affordability and current mortgage rates.

Bottom Line

For a more in-depth understanding of home price trends and reports, let’s connect.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link